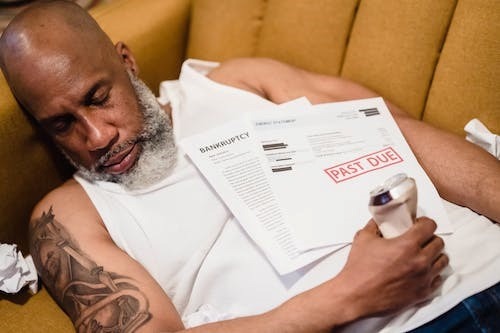

Managing personal finances can be a daunting task, and the fear of falling into bankruptcy is a nightmare for many. Bankruptcy can occur for various reasons, including unexpected job loss, medical expenses, overspending, or poor financial planning. Whatever the reason, the road to recovery and stability can be long and challenging. However, there are several ways to avoid bankruptcy and improve your financial situation. By taking proactive steps to manage your debt, negotiate with creditors, increase your income, and seek professional help, you can take control of your finances and avoid pitfalls. Want to know how? This article will explore some effective strategies to avoid bankruptcy and achieve financial stability.

1. Sell assets

When it comes to avoiding bankruptcy, liquidating your assets can be a viable option to conjure up some quick money to pay off debts. While auctioning off your prized possessions may be painful and may seem like you’re downgrading your lifestyle, studies have shown that owning fewer things can make you happier, not to forget it can streamline your financial situation. For instance, if you have an exotic car that you rarely use, selling it could be a smart financial move. A platform like DRIVERRA can help you sell your exotic car for cash quickly and easily without having to go through the hassle of finding a buyer. DRIVERRA provides a fast and reliable service tailored to meet the needs of exotic car owners. They offer a straightforward process for selling your car, which includes an online valuation, inspection, and immediate payment upon completion of the sale. By selling your assets through platforms like DRIVERRA, you can generate cash to pay off debts and put yourself on the path to financial stability.

2. Create a budget

Creating a budget is one of the most crucial steps in managing personal finances. A well-planned budget can help you stay on track financially and avoid overspending. A budget will outline your expected income and expenses over a specific period to provide you with a clear picture of your financial situation, so you can make informed decisions about your spending. Creating a budget can be a simple process involving tracking your income and expenses. You can use a spreadsheet or a budgeting app to keep track of your expenses and categorize them into essential and non-essential spending. By prioritizing essential expenses and reducing or eliminating non-essential spending, you can identify areas where you can cut back and save money.

Reviewing your budget regularly and adjusting as needed is important to ensure you stay on track to meet your financial goals.

3. Prioritize your debts

When managing debt, prioritizing is a smart strategy. Prioritizing debts means identifying which debts to pay off first based on their interest rates and the amount owed. High-interest debts, such as credit card debts, should be paid off first as they accrue more interest over time and can quickly spiral out of control. By focusing on high-interest debts, you can reduce the overall interest you pay over time.

Prioritizing debts can also help you make at least the minimum payment on all debts to avoid late fees and penalties. By creating a payment plan and sticking to it, you can steadily progress toward paying off your debts and achieving financial freedom.

4. Negotiate with your creditors

If you are struggling to keep up with your debt payments, negotiating with your creditors can be a smart move. It’s important to remember that at the end of the day, creditors want to get paid and are often willing to work with borrowers to develop a manageable repayment plan. You can start by contacting your creditors, explaining your financial situation, and asking if they can offer solutions, such as a lower interest rate, a reduced payment plan, or a debt settlement offer.

Negotiating with creditors can reduce the financial burden and avoid late fees and penalties. It’s important, to be honest and upfront about your situation and to follow through on any agreed-upon payment plans. By demonstrating a commitment to repaying your debts, you can build trust with your creditors and establish a positive track record for future financial endeavors.

5. Reduce expenses

To avoid financial trouble, reducing expenses is one of the most effective ways to achieve your financial goals. One approach to reducing expenses is creating a budget and tracking your expenses. This can help you identify areas where you can cut back, such as subscriptions or unnecessary purchases. You can also look for ways to save on everyday expenses, such as shopping for generic brands, using coupons, or taking advantage of sales.

Another way to reduce expenses is finding free or low-cost alternatives to expensive activities, such as entertainment, exercise, or travel. For example, instead of going to the movies, consider streaming movies or watching them at home. Additionally, you can cut down on transportation costs by using public transport, biking, or walking instead of driving. By adopting these approaches, you can reduce expenses, save money, and avoid bankruptcy.

6. Increase your income

Increasing your income can significantly improve your financial situation and help you pay off debts more quickly to avoid bankruptcy. There are several ways to increase your income, such as taking on a part-time job, freelancing, starting a side business, or pursuing additional education or training to qualify for a higher-paying job. It’s essential to choose an option that fits your skills, interests, and schedule and to be realistic about how much extra income you can earn.

It’s important to remember that increasing your income may require additional time and effort, but the payoff can be well worth it in the long run.

Conclusion

In conclusion, avoiding bankruptcy can seem daunting, but there are many steps you can take to stay afloat and avoid financial ruin. By selling assets, creating a budget, prioritizing debts, negotiating with creditors, seeking professional help, and increasing your income, you can stay on top of your finances and avoid the devastating effects of bankruptcy. These strategies require effort and commitment, but with patience and perseverance, you can overcome financial difficulties and build a brighter financial future. Remember, it’s never too late to take control of your finances and make positive changes toward achieving financial stability. By taking the necessary steps to avoid bankruptcy, you can safeguard your financial future and enjoy the peace of mind that comes with knowing you’re in control of your finances.